India’s smart metering market is experiencing significant momentum and transformation. Following the launch of several schemes by the government aimed at improving the distribution infrastructure, there has been an evident uptick in the demand and adoption of smart metering solutions across the country. Smart meters and smart grids hold immense potential to revolutionise the power sector through efficient monitoring of usage and faulty applications, swift interventions and grid stabilisation. Smart grids are characterised by their advanced solutions and utility benefits ranging from optimised asset utilisation and reduction in transmission and distribution losses to peak load management and increased grid visibility.

Launched in 2022, the Ministry of Power’s Revamped Distribution Sector Scheme (RDSS) initiative aims to improve the operational efficiency and financial sustainability of discoms. The RDSS has two components: Part A for financial support in prepaid smart metering, system metering and distribution upgrades; and Part B for training, capacity building and support activities. The outlay for smart metering is Rs 1,349.86 billion, while for loss reduction, it is Rs 1,191.34 billion. The scheme includes plans to install 250 million prepaid smart meters with an outlay of Rs 1,500 billion and budgetary support of Rs 230 billion. System metering at feeder and transformer levels with advanced metering infrastructure (AMI) will enable automatic energy measurement. Smart meter roll-out will be facilitated through public-private partnerships in the total expenditure mode, enforcing service-level agreements for proper energy accounting, identifying defaulting consumers and preventing meter tampering. Prepaid metering is expected to enhance revenue from improved billing and collection, helping discoms fund monthly costs.

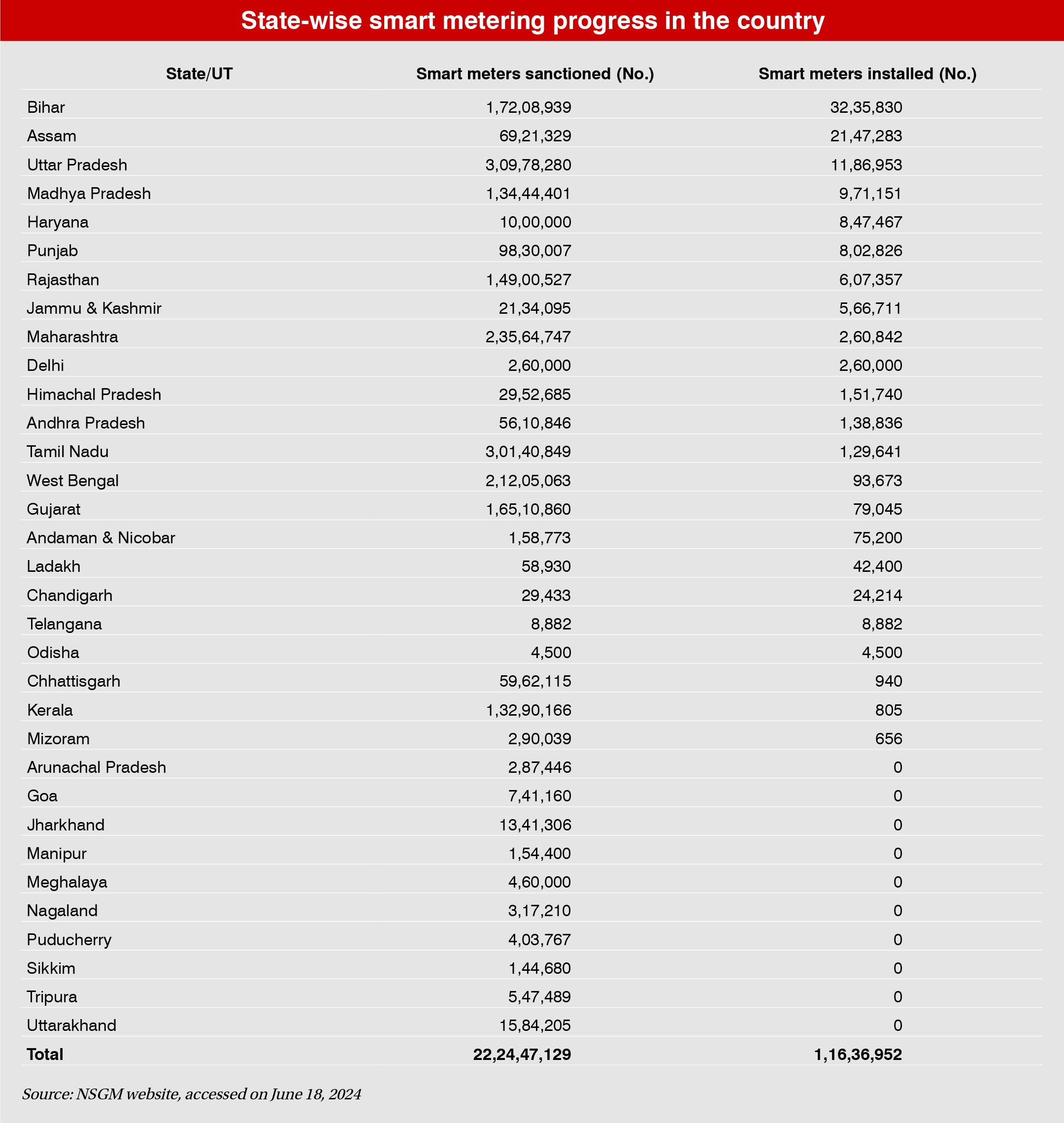

Smart metering progress so far

Approximately 222 million smart consumer meters, 5.26 million distribution transformers (DT) meters and 0.18 million feeder meters have been sanctioned across the onboarded states. As of June 2024, over 117 million consumer smart meters have been awarded, which is 53 per cent of the total sanctioned meters, and 11.6 million consumer smart meters have been installed till date as per the National Smart Grid Mission (NSGM) dashboard. Further, 4 million DT meters or 77 per cent of the sanctioned meters and 130,295 feeder smart meters or 71 per cent of the sanctioned meters have been awarded.

Notably, during 2023-24, 4.84 million smart consumer meters have been installed, nearly double the installations from the previous year. With the government mandating the transition to a complete smart metering system, replacing all the existing 250 million meters by 2025, the pace of smart meter awards and installations is expected to accelerate in the coming months. Bihar leads with the highest number of installed smart meters, totalling 3,235,830, followed by Assam with 2,147,283 installed. Uttar Pradesh closely trails with 1,186,953 meters installed, while Madhya Pradesh and Haryana have installed 971,151 and 847,467 meters respectively.

Under the smart grid pilot projects, as of May 2024, 24,214 smart meters have been installed by the Chandigarh Electricity Division in Subdivision 5, while Jaipur Vidyut Vitran Nigam Limited has installed 145,343 smart meters to cater to 0.15 million consumers. The project entails the deployment of smart meters, AMI, distribution transformer monitoring units and supervisory control and data acquisition (SCADA) systems. The progress in the implementation of smart grid initiatives reflects significant strides in enhancing the efficiency and reliability of the power distribution system. Building on the successful completion of 11 smart grid pilots under the Restructured Accelerated Power Development and Reforms Programme, these projects have tested and validated a range of advanced technologies. The pilots, encompassing smart metering, radio frequency/power line communication/GPRS communication, peak load management, distribution transformer monitoring units, net metering, outage management systems and rooftop solar integration, showcase a holistic approach to grid modernisation. The integration of the metering, billing and collection system with AMI/smart metering underscores the seamless synergy between billing systems and cutting-edge metering technologies.

Opportunities

Opportunities

The smart grid initiative presents numerous opportunities, driven by the government’s commitment to providing 24×7 quality, reliable and affordable power for all. With universal access already achieved, the focus is now on enhancing the quality and reliability of power supply while building operational efficiencies and prioritising consumer centricity. Efforts are under way to scale up electric vehicle (EV) penetration, renewable energy integration and energy storage. The integration of renewable energy sources such as solar PV and wind, along with the penetration of EVs into the smart grid system presents immense opportunities. The integration of such technologies with smart meters would reduce the reliance on fossil fuels and the emission of greenhouse gasses into the environment. Smart grid energy storage technologies such as plug-in hybrid electric cars, battery energy storage systems, energy storage systems and plug-in EVs are also increasingly gaining more proficiency. The adoption of new and emerging smart grid technologies is being actively promoted, supported by the developed ecosystem and knowledge dissemination efforts by NSGM. Sustained intervention is essential for the successful implementation of RDSS, incorporating AMI, artificial intelligence and machine learning to realise the futuristic visions for 2030 and 2047.

Challenges

A host of issues and challenges have been hindering the widespread deployment of smart meters. A key challenge has been IT system integration and interoperability. There are complexities in ensuring seamless integration and interoperability among different hardware and software components from various vendors. Further, the lack of standardised protocols and interfaces leads to compatibility issues between smart meters, network interface cards and communication networks. The complex integration between the utility IT system and meter data management systems also causes delays and increases costs.

In addition, the risk of the technology becoming outdated or no longer supported over the duration of the contract can create compatibility issues, increase maintenance costs and limit functionality. Network challenges encompass unreliable networks, which create latency and congestion problems and increase the cost and dependency on telecom operators.

Handling removed meters presents its own complications, such as the lack of a standard operating procedure for managing and disposing of static meters, resulting in inefficient utilisation of resources. Further, obstacles posed by the lack of smart meter adoption by utility officials, along with inadequate training and capacity-building, hinder the ability to derive meaningful insights from data and translate them into actionable decisions. Finally, challenges exist in integrating data-driven insights into decision-making processes effectively. Without clear mechanisms for incorporating analytics findings into strategic planning, operational workflows and policy formulation, the full potential of smart metering technology may remain unrealised.

Way ahead

The next phase of smart metering will focus on smart distribution. Implementing a smart grid will increase reliability, improve service quality, enhance safety and create resilient distribution networks. It will significantly boost operational efficiency, enhance consumer centricity, and support better decision-making and planning. The grid is also aiming for flexibility and scalability to future-proof utilities. Expected outcomes include reduced outages, improved reliability indices (system average interruption duration index, system average interruption frequency index, customer average interruption duration index and customer average interruption frequency index), and decreased unserved energy. The smart grid is anticipated to enhance billing and collection efficiency, reduce aggregate technical and commercial losses, and narrow the average cost of supply-average realisable revenue gap. It will also minimise accidental risks, integrate renewable energy better, and boost consumer engagement and satisfaction. Additional benefits include value-added services, improved asset utilisation, lower power procurement costs and adaptive tariff structures such as critical peak pricing.

Smart distribution technologies will be implemented in two phases. Phase I (until 2026) includes DT and feeder metering, and AMI and consumer indexing. It will aim for 50 per cent coverage, with 100 per cent by Phase II (2030). SCADA, distribution management and outage management systems will be set up at 33 kV and 11 kV levels and for critical DTs, with plans for future expansion. Distribution infrastructure improvements such as underground lines and gas-insulated switchgear substations will be based on network needs in both phases. Asset mapping will start at substations and feeders, and then move to low tension lines and consumers. Initial DT monitoring will cover 10 per cent of DTs, with plans to scale up. Smart streetlighting will involve retrofits and new installations in Phase I, with more deployments in Phase II. Data analytics for consumers and low voltage networks will start with pilot projects. Smart energy storage and charging stations will also undergo pilot testing before scaling. Drone-based asset management will initially be implemented for the 33 kV network, followed by 11 kV. Flexibility services, including time-of-use and demand response, will start as pilot projects and expand. The distributed energy resources (DER) management system and peer-to-peer energy trading will be piloted in DER-rich areas before wider implementation in Phase II.

Overall, as the country’s energy consumption continues to rise, the need for adopting advanced technologies in smart meter distribution infrastructure becomes paramount. Looking ahead, the integration of such innovative solutions will be pivotal in augmenting operational efficiency, enhancing consumer centricity and improving decision making.

Based on a presentation by Atul Bali, director, NSGM, at a recent Power Line conference